Starting a medical practice can be stressful.

And like any business, figuring out where, and how, to get the capital you need to keep going can be the most stressful part.

Especially so in the medical field when you have thousands of dollars in student loans hanging over your shoulder.

The good news is that there are several great options when it comes to funding your medical practice.

In today’s blog, we’re going to cover the best loan options for your medical practice and point you in the right direction to get started.

Let’s dive in.

What is a Medical Practice Loan?

First things first, what is a medical practice loan?

A medical practice loan provides necessary funding for new and existing medical service businesses.

The qualifications for medical practice loans are typically based on the health of the medical practice,

as well as the individual professional’s credit worthiness.

However, there are loans specially geared towards doctors and dentists that take into consideration unique circumstances, such as thousands of dollars accumulated in debt.

What is a Medical Practice Loan?

When it comes to the type of medical practice loan you should take out – there are several great options to choose from.

Here are a few of the ones to consider:

- A Business Line of Credit: A business line of credit gives you access to flexible, revolving funds when you need them for your practice. With a line of credit, you borrow what you need, pay down the balance, and the funds are replenished so you can use the line again.

- A Short-Term Business Loan: With terms that range from three months to three years, this type of financing makes it possible for a doctor’s office to borrow capital and repay it quickly.

- Equipment Financing: Equipment financing is another way to finance the purchase of business equipment. For medical practice owners, business equipment can include autoclaves, x-ray imaging equipment, computers, and diagnostic tools like medical scales and ECG monitors.

- A Bank Loan: A bank loan typically requires collateral to secure the loan, and the application process tends to take several weeks.

- The SBA (Small Business Administration) Loan Guarantee Program: If your medical practice is an established business, with a few years under its belt, and your personal credit score is above 680, this could be an option for your practice.

Two Best Loan Options for Medical Practices

When it comes to the best loan options for medical practices, there are two we recommend the most.

However, it’s important to note that the best loan option for your medical practice will always depend on your unique situation.

We recommend getting in touch with an experienced medical accountant to help you weigh your options and choose the most advantageous option.

This is an important decision, and it’s always best to bring in a knowledgeable expert.

SBA 7(a) Loans

The first loan type we recommend for doctors and dentists is a Small Business Administration, or SBA loan.

An SBA loan is a great option for doctors and dentists because of its flexibility and terms. SBA loans carry some of the lowest interest rates and longest repayment terms on the market.

Additionally, due to the financial security of being a doctor or dentist – higher wages, high credit scores, and steady income – both professions are typically strong candidates for this competitive loan.

However, if you’re just starting your practice for the first time, an SBA 7(a) loan might not be the best option. The most qualified borrowers not only have strong credit scores, but also a few years of experience in business under their belt, too.

Business Line of Credit

The next loan option for medical practices we recommend is a business line of credit.

A business line of credit operates differently to the typical bank loan you’re used to. In fact, it operates more like a business credit card.

A lender will approve you for a set amount, and you’re able to quickly access the funds when and where you need it.

It’s essentially a safety net to have in your back pocket for fluctuating expenses or big equipment purchases.

Given its flexibility and cost-effectiveness, the business line of credit is widely considered among the best medical practice loans for doctors and specialists—regardless of what stage of the business you’re in.

Where Can Medical Practitioners Borrow Funding From?

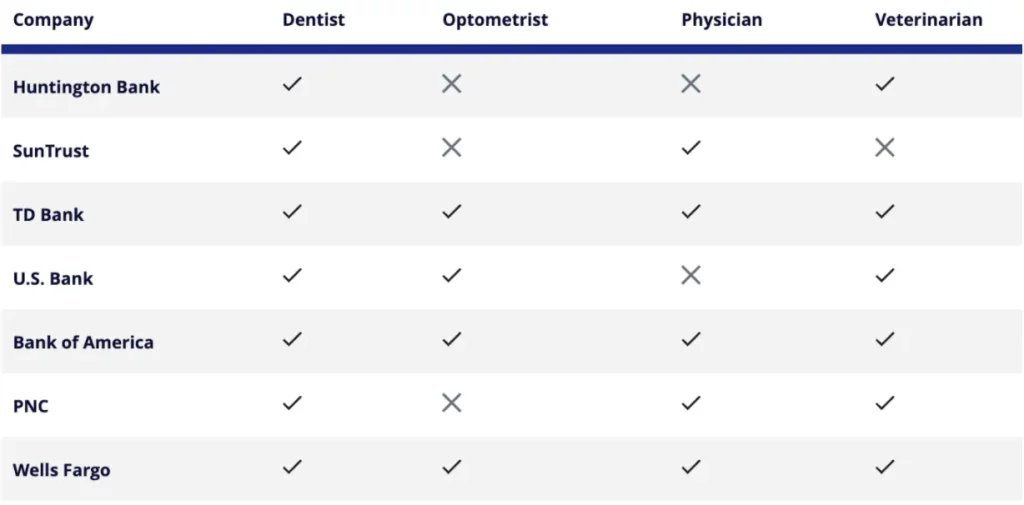

To keep things simple, here’s a quick list of banks to look into for your medical practice loan:

Chart Credit: Business.org

- Huntington Bank – Huntington Bank offers financing for veterinarians and dentists. Its practice funding options include everything from startup loans to equipment financing to debt refinancing.

- SunTrust (Best for Recent Graduates) – What really makes SunTrust stand out is the fact that it lends not just to current doctors but also to doctors in training. Fourth-year med students and residents can qualify for SunTrust doctor loans—no need to wait until after graduation.

- TD Bank- While lots of lenders let you buy an existing practice, TD Bank is one of the few that calls out buying into a partnership or buying out a partner—similar, but distinct from, simply buying a practice.

- U.S. Bank- U.S. Bank emphasizes funding existing practices—acquiring, buying into, expanding, and relocating them. It doesn’t offer loans for starting up a brand-new practice; if that’s your goal, go with a different lender.

- Bank of America- When you fund a practice through Bank of America, you get a project manager who is dedicated to your business. They’ll use their expertise to help you do your project right—and within your budget and time constraints. You’ll even get specialized market analysis for your practice.

- PNC- PNC offers tons of expert advice and guidance through its resources for practices. That kind of expertise means PNC can understand your practice’s needs and help you select the right funding (and other products) to help it grow.

- Wells Fargo- Wells Fargo hosts its own practice marketplace where you can buy or sell an existing practice. We’ve seen everything from a $10,000 dental practice in Danville, CA, to a $1 million medical practice in Los Angeles.

What To Do Next?

The #1 thing we recommend doing before borrowing money for your medical practice is to consult with your medical accountant.

An experienced medical practice can help you weigh the pros and cons of taking out a business loan, and help you choose the most economic option for your situation.

If you don’t currently have a dedicated medical accountant, you can book a free consultation with one of our accountants at any time. We’re always here to help.